Step-by-step guide for new drivers after a car accident. From safety to insurance claims to talking to police.

Your heart is pounding. There's broken glass on the road. Another car is stopped in front of you. And you have no idea what to do.

This is the moment that separates new drivers from prepared drivers.

It's not panic—panic is natural. It's what you do in the first 30 seconds, the next 10 minutes, and the hours that follow that will determine whether you're protected legally and financially, or whether small mistakes become expensive regrets.

Most new drivers make at least one mistake at an accident scene: they admit fault before the facts are clear, they fail to document the scene, they give a recorded statement to the other driver's insurance company (which can be used against them later), or they simply walk away without gathering critical information.

This guide walks you through every step of handling an accident—from ensuring safety, to talking to police and witnesses, to navigating the insurance claim process—so that when (not if) it happens, you know exactly what to do.

Key Takeaways

- Safety first, blame second: Get to a safe location and check for injuries before worrying about the accident itself

- Never admit fault at the scene, even if you think the accident was your fault; let insurance investigations determine liability

- Document everything: Photos, witnesses, police report number, and driver/vehicle information are critical and protect you legally

- Your insurance company works for you, not the other driver's insurer. Know the difference before giving statements

- Accidents are stressful and expensive but are also learning opportunities. Wheelingo's defensive driving modules help you develop the judgment and situational awareness to avoid them

- As a new driver, your insurance rates will spike after an at-fault accident; understanding the claims process helps you minimize the damage

Step 1: Ensure Safety (First 30 Seconds)

Your immediate priority is preventing further injury.

Check for Injuries

- Are you hurt? If you're in pain, bleeding, or feeling dizzy, call 911 immediately. Don't drive to the hospital; let paramedics assess you.

- Check your passengers. If anyone else is in your car, ask if they're okay. Don't move someone who's injured unless there's immediate danger (fire, oncoming traffic).

- Check the other vehicle (if safe). If you can approach the other car without putting yourself in traffic, knock on the window and ask if anyone needs help.

Move Vehicles to Safety (If Possible)

- If both cars are drivable and traffic is moving, move to the shoulder or parking lot, away from active traffic lanes. Staying in the middle of the road invites a third car to hit you.

- If a vehicle is disabled or heavily damaged, turn on hazard lights and leave it where it is. Trying to move it could worsen injuries or damage evidence.

- If you're on a highway, get out of traffic and behind your vehicle if it's safe. Don't stand in a traffic lane.

- If a vehicle is smoking or on fire, evacuate immediately and call 911. Do not stay nearby.

Turn on Hazard Lights

Even if you're moving the vehicles, activate your hazard lights immediately. This warns other drivers.

Step 2: Call 911 (When Appropriate)

Call 911 if:

Call 911 if:

- Anyone is injured

- There's significant damage to either vehicle

- You hit a cyclist or pedestrian

- There's a fuel leak or fire

- You hit parked property (like a parked car or storefront)

- A driver appears intoxicated or impaired

- A driver leaves the scene (hit-and-run)

- You feel unsafe or threatened

Don't call 911 if:

- Everyone is fine

- Damage is minimal (small dent, minor bump in a parking lot)

- You're in a safe location and can exchange information without police

In most states, you're required by law to report accidents involving injury or significant property damage. Failing to report can result in criminal charges.

What to Tell 911

Keep it simple and factual:

- "There's been a car accident on [road name] near [cross street or landmark]."

- "There are [X] vehicles involved."

- "No injuries / [number] people are injured."

- Confirm your exact location.

Don't speculate about fault or blame. Just provide the facts and location.

Step 3: Exchange Information with the Other Driver (First 10 Minutes)

Once you've ensured safety, exchange information with the other driver. Write everything down.

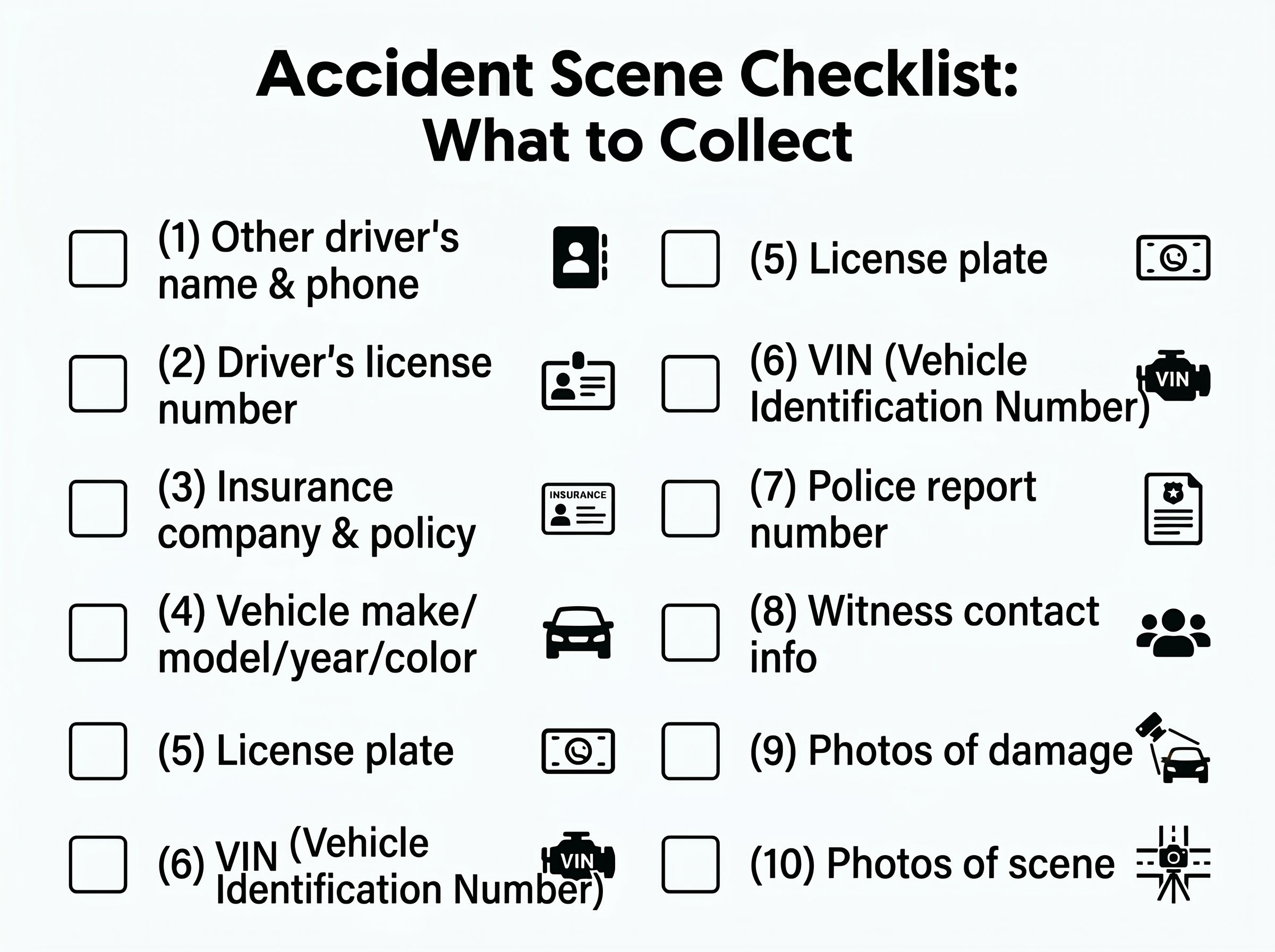

Critical Information to Collect

| Information |

Why It Matters |

| Full name and phone |

Contact for insurance and follow-up |

| Driver's license number |

Identifies the driver; confirms licensure |

| Address (current) |

For mail, legal documents |

| Insurance company and policy number |

Required to file a claim |

| Vehicle make, model, year, color |

Identifies the vehicle and insurance coverage |

| License plate number |

Identifies the vehicle legally |

| VIN (Vehicle Identification Number) |

Critical for insurance and accident reconstruction |

How to Collect This Information

- Ask to see their driver's license and photograph it (front and back). Don't accept a verbal recitation.

- Ask to see their insurance card and photograph the front and back.

- Take a photo of their license plate.

- Ask for their cell phone number in case insurance needs to reach them.

- Get their email address (for documentation).

Do not:

- Accept a handwritten phone number you can't verify

- Skip getting their insurance information

- Rely on memory; photograph everything

Step 4: Document the Accident Scene (Critical Step)

Photos are evidence. They protect you. Take as many as possible.

Photos are evidence. They protect you. Take as many as possible.

Photos You Need

- Overall scene: Wide shots of both vehicles at the accident location, showing road conditions, traffic signals, and surrounding environment.

- Damage to both vehicles: Close-ups of all visible damage on each vehicle, from multiple angles.

- Vehicle positions: Show where each vehicle came to rest relative to the road, curb, and traffic signals.

- Skid marks or debris: If visible, photograph any skid marks, broken glass, debris, or other evidence on the road.

- Traffic signs and signals: Photo of relevant traffic signals, stop signs, or speed limit signs.

- Time and location: If possible, use your phone's GPS to mark the location, or note the street address.

What NOT to Photograph

- Do not photograph the other driver's face (privacy, liability).

- Do not take video of the other driver or passengers without consent (privacy laws).

- Do not photograph anything that incriminates you (e.g., if you're texting and driving, don't let the phone be visible).

Use Your Phone's Timestamp

Most phones automatically timestamp photos. This proves when the photos were taken, which is important for documentation. Check that your phone's date and time are correct.

Step 5: Get Witness Information

If anyone saw the accident, get their contact information immediately. Witnesses are invaluable if there's a dispute about fault.

Witness Information to Collect

- Full name

- Phone number

- Email address

- Home address (optional, but helpful)

- What they saw (brief, no need to get a full statement)

- Relation to either driver (friend, bystander, etc.)

Why it matters: If the other driver later claims you ran a red light and you have a witness who says you didn't, that witness can be contacted by your insurance company or attorney.

Step 6: Talk to Police (If They Arrive)

In many cases involving significant damage or injury, police will respond and investigate.

What to Expect

- Officer arrives and assesses safety, checks for injuries.

- Officer asks for your driver's license, registration, and proof of insurance.

- Officer may ask you to describe what happened. Answer honestly and factually, but don't speculate or assign blame.

- Officer interviews the other driver and witnesses.

- Officer fills out a police report and provides you with a report number.

What to Say

Be honest, brief, and factual. Example:

Officer: "What happened?"

You: "I was driving north on Main Street. The light turned green. I entered the intersection. The other vehicle was already in the intersection and hit the passenger side of my car."

That's it. You're not assigning blame (maybe the other driver's light had been green longer and they had right of way; maybe they ran the light—let the facts speak). You're just describing what you observed.

What NOT to Say

Do not:

- Admit fault: "I wasn't paying attention." "I didn't see them."

- Apologize in a way that implies fault: "I'm so sorry, it's my fault."

- Speculate: "I think they were on their phone."

- Lie: Never lie to a police officer. It's a crime and undermines your entire case.

- Get angry or defensive: Stay calm and respectful.

Get the Police Report Number

Before the officer leaves, ask for the report number. You'll need this to file an insurance claim.

Officer: "Your report number is [XXXXX]. You can obtain a copy at [police station/website] in [timeframe]."

Write this down or take a photo of the officer's card.

Step 7: Don't Sign Anything at the Scene

A common mistake: signing a document the other driver or a third party presents at the scene.

Don't sign:

- Admissions of fault

- Medical authorization forms (presented by the other driver)

- Settlement agreements

- Anything you haven't read carefully

The only documents you should consider signing:

- Police report paperwork (if the officer requests it)

- Your own insurance agent's documentation

When in doubt, tell the other party, "I'll have my insurance company contact you," and don't sign anything.

Step 8: Contact Your Insurance Company (Within 24 Hours)

This is critical. Most insurance policies require that you report an accident promptly.

What to Tell Your Insurer

- You were involved in an accident.

- The date, time, and location.

- No one was injured (or extent of injuries, if applicable).

- Brief description of what happened (factual, no admission of fault).

- The police report number (if one was filed).

- The other driver's name, phone, and insurance info.

- Whether you have photos or witness information.

What NOT to Tell Your Insurer

- Do not admit fault: "It was totally my fault."

- Do not speculate: "I think I was speeding, but I'm not sure."

- Do not make up details you don't remember.

Your insurer is on your side. Be cooperative and factual. Let them investigate.

About Recorded Statements

Your insurance company may ask for a recorded statement about the accident. This is fine—they're allowed to. But:

- Do not give a recorded statement to the other driver's insurance company without consulting your own insurer first or speaking to an attorney.

- If the other driver's insurer calls and asks for a statement, say: "I'll have my insurance company contact you. Please send your request in writing."

- A recorded statement given to the other driver's insurer can be used against you if there's a dispute.

Step 9: Document Medical Issues (If Any Injuries)

Even if you feel fine, some injuries develop over days or weeks.

Seek Medical Attention

- If you're in pain or feel unwell, see a doctor within 24–48 hours of the accident.

- Get documentation of your visit and any diagnosis.

- Follow up if symptoms worsen. Neck or back pain (whiplash) can appear days later.

Tell Your Doctor

- You were in a car accident.

- Date and general description.

- Any pain, numbness, or unusual symptoms you've experienced since.

The medical record documents your injuries for the insurance claim and establishes that any health issues are related to the accident, not a pre-existing condition.

Real Scenario: How a New Driver's Accident Unfolds

Scenario: The Rear-End Accident

Timeline:

- 2:15 PM: Tyler, 19, is driving home from work. He stops at a red light. Another car, driven by a 25-year-old, hits Tyler's car from behind at about 15 mph.

- 2:16 PM: Tyler's heart is pounding. The other driver gets out. "Are you okay? I didn't see the light turn red."

Tyler's mistake: Hearing the other driver admit fault, Tyler says, "Yeah, it's okay, no biggie." He accepts the other driver's offer to just exchange contact info and settle it later.

2:20 PM: Both drivers exchange information and leave the scene.

2:45 PM: Tyler's neck starts to hurt—whiplash from the impact. He doesn't think it's serious.

3:30 PM: Tyler finally calls his insurance company and reports the accident. He mentions that "the other driver said they didn't see the light," but doesn't get a police report (he didn't call 911).

4:00 PM: Tyler takes photos of the damage to his car—but only now, two hours later, when debris and evidence may have been cleared.

What went wrong:

- Tyler didn't immediately call 911 (if there was any injury, reporting is legally required).

- Tyler didn't call police for a report (without an official report, establishing fault is harder).

- Tyler didn't document the scene immediately.

- Tyler didn't get witness info (there may have been cars around).

- Tyler didn't seek medical attention immediately (whiplash is documented better when reported early).

The consequences:

- Tyler's insurance rates spike 25% for three years because he's now on record as an at-fault driver (the other driver later disputes their admission and claims Tyler ran the red light; without a police report, it becomes he-said-she-said).

- Tyler's medical claim for whiplash is weaker because he didn't seek immediate medical attention (the insurer questions the severity).

- Tyler repairs his car (his deductible: $500; repair cost: $3,200; insurance pays $2,700).

- Three years of increased premiums: $250/year × 3 = $750.

Total cost: $500 (deductible) + $750 (insurance increase) = $1,250, plus ongoing inconvenience and higher premiums after.

What Tyler Should Have Done

- Called 911 immediately (even if injuries seemed minor).

- Waited for police to arrive and complete the report.

- Documented the scene with photos of damage, location, and vehicles.

- Got witness information from any nearby drivers or pedestrians.

- Sought medical evaluation at an urgent care within 24 hours, even though pain seemed minor.

- Called his insurance company within 2 hours with all information gathered.

- Did not accept cash settlements or promises from the other driver.

By following these steps, Tyler would have a documented police report, medical records establishing injury, and witness corroboration—making his insurance claim much stronger.

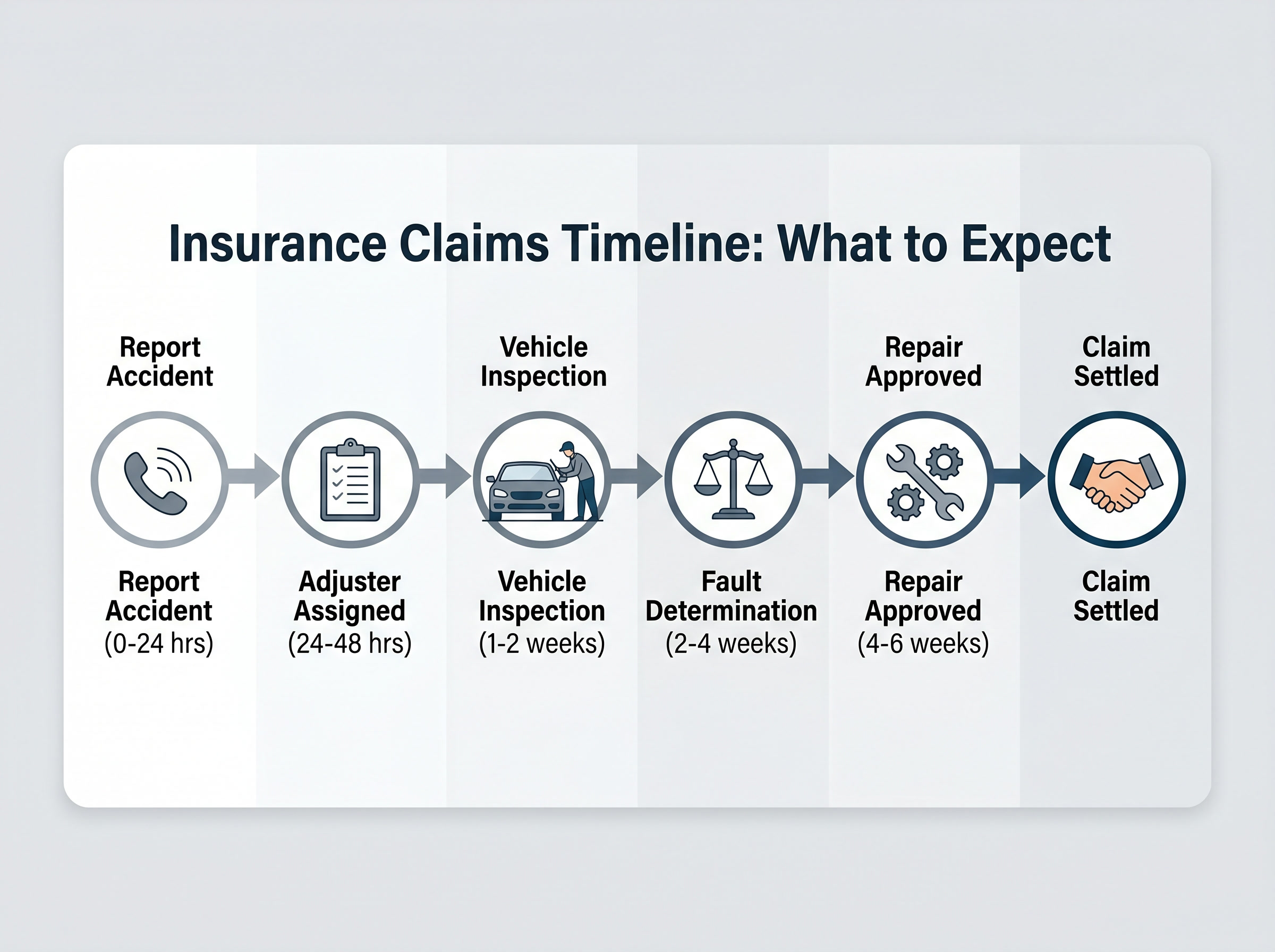

Insurance Claims: What Happens Next

After you report the accident, here's how the claims process typically unfolds:

| Timeline |

What Happens |

| 0–24 hours |

You report accident to your insurer |

| 24–48 hours |

Insurer opens a claim file, assigns adjuster |

| 48 hours – 1 week |

Adjuster reviews details, may contact other driver |

| 1–2 weeks |

Adjuster inspects vehicle damage, gets repair estimates |

| 2–4 weeks |

Insurance determines fault (yours, other driver's, or shared) |

| 4–6 weeks |

Repairs approved, claim paid (less deductible if at-fault) |

| 6+ weeks |

Additional negotiations if dispute about fault or damage |

At-Fault vs. Not-at-Fault Claims

- At-fault: You're responsible; you pay your deductible; your rates increase.

- Not-at-fault: The other driver is responsible; you pay nothing (or lower deductible); your rates may not increase or increase minimally.

- Shared fault: Liability is split; rates may increase modestly.

State laws vary on how fault is determined and how it affects rates, but the general rule is: at-fault accidents = higher premiums for 3–5 years.

Start Practicing Today

The fastest way to pass your test is consistent practice with real questions. Try Wheelingo free — state-specific questions, instant explanations, and a readiness score that tells you when you're ready.

FAQ: Car Accidents for New Drivers

Q: Should I move my car out of the road if it's blocking traffic?

A: Only if it's safe and the car is drivable. If you're worried about other cars hitting yours, prioritize safety and pull to the side. However, if the car is heavily damaged, leave it and turn on hazards. Call 911 if you need help managing traffic.

Q: What if the other driver doesn't have insurance?

A: Document their information anyway. Your own insurance has coverage for uninsured motorists (in most states). Report the accident to your insurer with the other driver's information, and your uninsured motorist coverage will cover your damages (you still pay your deductible).

Q: Can the other driver sue me after an accident?

A: Yes. If they claim injury and your insurance denies liability, they can pursue a personal injury lawsuit. This is why documenting the accident and getting a police report is important—it's evidence if the case goes to court.

Q: Should I post about the accident on social media?

A: Absolutely not. Do not post photos, descriptions, or comments about the accident on Facebook, Instagram, TikTok, or any social platform. Anything you post can be used against you in a claim or lawsuit. Delete any posts about the accident from years past.

Q: How long will the accident affect my insurance rates?

A: Typically 3–5 years, depending on your state and insurer. Some states allow accidents to be dropped off your record after 3 years; others keep them for 5. Serious accidents or repeat offenses can affect rates longer.

Q: If I'm a teen driver with a learner's permit, does my parent's insurance cover me?

A: Usually yes, as long as you're listed on the policy. However, an at-fault accident will increase the rates for the entire household, not just you. Discuss with your parent or guardian before driving.

Q: What if a police officer shows up and says it's my fault?

A: Don't accept the officer's preliminary fault determination as final. Insurance companies investigate independently. An officer might say, "It looks like you didn't see the other vehicle," but that's preliminary. Let your insurance investigate.

Q: Do I need a lawyer after an accident?

A: Not always. If injuries are minor and the accident is straightforward, your insurance company will handle it. If injuries are significant, the other driver is suing, or there's a major dispute about fault, consult a personal injury attorney (many work on contingency, meaning you pay only if you win).

Defensive Driving: Avoid Accidents Before They Happen

The best accident is the one you prevent. Wheelingo's defensive driving practice teaches you to:

- Recognize high-risk situations before they escalate (car weaving, running lights, aggressive driving).

- Maintain safe following distance (3+ seconds behind the car ahead).

- Anticipate other drivers' moves and position yourself defensively.

- Manage your own distractions (phone, eating, adjusting radio).

- Drive for the conditions (slow down in rain, fog, or heavy traffic).

These skills reduce your crash risk dramatically. And fewer accidents mean lower insurance rates, less stress, and a safer driving record for years to come.

Conclusion: Accidents Happen, But Preparation Prevents Panic

Every driver will eventually be involved in an accident. The question isn't if—it's when. And when it happens, the drivers who are prepared are the ones who protect themselves legally and financially.

You now have a step-by-step guide to follow. Print it. Memorize it. Teach it to friends. When an accident happens—and you're shaken and confused—you'll know exactly what to do.

Safety → Documentation → Information Exchange → Police Report → Insurance Notification.

Follow that sequence, stay calm, and you'll get through it.

And remember: the best accident is the one you prevent. Drive defensively. Stay focused. Make it home safe.

Related Articles:

Sources & Further Reading: